You Have Gold. Now You Need Cash.

Nobody talks about the selling side. Here's how turning gold back into dollars actually works — and what it costs.

Nobody talks about this part.

Every gold blog, every YouTube channel, every Reddit thread — it's all about buying. What to buy, when to buy, how much premium is too much. And look, that stuff matters. But at some point, life happens. Maybe it's a down payment on a house. Maybe it's a medical bill. Maybe you just want to lock in profits after a monster run.

Whatever the reason, you're sitting there with gold in your hand and you need dollars in your account. And suddenly you realize: you have no idea how this actually works.

I've been there. I've also been on the selling side of the table — I've minted product, I've moved metal, I've watched people walk into shops with no clue what their gold was worth and walk out with 70 cents on the dollar. That's what this post is about. Making sure that doesn't happen to you.

First, the Uncomfortable Truth

Gold is liquid. It's one of the most liquid assets on the planet. Central banks hold it for exactly this reason.

But “liquid” and “instant” are not the same thing. And “liquid” and “no friction” are definitely not the same thing.

When you sell gold, you're going to lose something on the transaction. That's just how it works. The question is how much you lose, and that depends almost entirely on which path you take.

Let me walk you through the options, from worst to best.

Pawn Shops: Just Don't

I'll keep this short because the answer is simple. Don't.

Pawn shops are in the business of buying things from people who need money right now and have no other options. Their entire model depends on paying you significantly less than what your stuff is worth. We're talking 50–70% of melt value on a good day. On a bad day? I've heard worse.

They're not trying to rip you off — well, some are — but even the honest ones have overhead, risk, and a business model that requires massive margins on every transaction.

If you're reading this, you have other options. Use them.

Local Dealers: The Most Common Route

This is where most people end up, and honestly, it's not a bad choice if you know what you're doing.

Here's how it typically works. You walk in with your gold. They test it (XRF gun, acid test, whatever their setup is). They check the day's spot price. They make you an offer.

That offer is going to be below spot. How far below depends on a few things:

What you're selling matters a lot. Generic bars and rounds from well-known refineries? They'll pay close to spot, sometimes even at spot. Government-minted bullion coins often command a small premium even on the sell side. Random jewelry or unmarked bars? Expect a bigger haircut because they have to verify and possibly refine it.

The dealer's inventory matters. If they're already sitting on a pile of whatever you're bringing in, they have less incentive to buy yours. If they're low on stock or there's strong local demand, you'll get a better price.

Your relationship matters. This sounds old-school, but it's real. Dealers who know you, who've sold to you before, who trust that your stuff is legit — they'll give you tighter spreads. Walk in cold and you're starting from zero.

- Call ahead. Don't just show up with a tube of coins and expect them to have cash on hand. Especially for larger amounts.

- Get multiple quotes. Visit two or three dealers if you can. Spreads vary more than you'd think.

- Know the spot price before you walk in. Check it that morning. Know what melt value is for exactly what you're carrying. If a dealer is offering you 10% below melt on standard bullion, you can do better.

- Bring documentation. Original receipts, certificates of authenticity, anything. It speeds up the process and builds trust.

Typical buyback on standard bullion at a decent local dealer: somewhere between spot and 2–3% below spot. On generic rounds and bars, maybe 3–5% below. That's the realistic range.

Online Buyback Programs: Convenient, but Read the Fine Print

Most major online bullion retailers run buyback programs. The process is usually: you get a quote on their website or over the phone, you lock in a price, they send you a shipping label, you mail your gold (insured), they verify it, and then they send you a check or wire.

Sounds clean. And it can be. But there are things to watch for.

The lock-in window is tight. When they quote you a price, that quote is good for a very limited time — sometimes hours, sometimes until market close that day. If you don't ship within their window, the price resets. This makes sense from their side (they're hedging against price movement), but it means you need to be ready to act.

Shipping is a thing. You're putting gold in a box and handing it to a carrier. Yes, it's insured. Yes, people do it every day. But it's still a layer of risk and delay that doesn't exist when you walk into a local shop and walk out with cash.

Verification adds time. Even after they receive your package, there's a processing window before you get paid. Could be a few days, could be longer.

Their quoted spreads look good on paper. And they often are competitive — sometimes better than local dealers, especially for common bullion products. But factor in the time value of your money sitting in transit and processing, and the gap narrows.

Online buyback works best for larger transactions where the slightly tighter spread justifies the hassle, and for people who don't have a good local dealer nearby.

Peer-to-Peer: Best Price, Most Work

Selling directly to another stacker — whether that's through forums, local meetups, or the various online communities where metals change hands — will almost always get you the best price. You're cutting out the middleman entirely.

Sellers in peer-to-peer markets can often get spot or even slightly above for desirable products. Buyers are happy because they're paying less than retail. Everybody wins.

But.

There's friction. You need to find a buyer. You need to establish trust (or use an escrow mechanism). You need to handle shipping and insurance yourself if it's not local. And there's always some level of scam risk — on both sides.

- Reputation is everything. The more transaction history you have in a community, the easier every subsequent sale becomes. If you've never sold before, start small.

- Be specific in your listings. Weight, purity, product type, year, condition. Photos with timestamps. The more transparent you are, the faster you sell.

- Payment method matters. Some payment methods are reversible (and therefore risky for sellers). Know which ones protect you.

- Meet in safe locations for local deals. Bank lobbies, police station parking lots. This is not paranoia, it's common sense when you're carrying gold.

Peer-to-peer is the best option if you have the time, the reputation, and the risk tolerance. It's the worst option if you need cash tomorrow.

Gold-Backed Debit Cards: The New Option

This is the most recent development and honestly, it's interesting.

A few platforms now offer debit cards linked to your gold holdings. The idea is simple: instead of selling your gold and then spending dollars, you spend and the platform sells a corresponding amount of gold to cover the transaction in real-time.

In theory, this is great. You get the liquidity of cash with the storage of gold. No need to find a buyer, no shipping, no negotiating.

In practice, there are things to think about:

- Fees. Transaction fees, card fees, spread fees on the gold-to-cash conversion. These add up. Read the fee schedule carefully.

- Tax implications. Every time you “spend” gold through one of these cards, you're technically selling gold. That's a taxable event. If you've held that gold for less than a year, you might be looking at short-term capital gains rates. If you've held longer, long-term rates — which are better, but still not zero. Tracking your cost basis across dozens of small card transactions sounds like a nightmare.

- Counterparty risk. Your gold is stored with the platform. You're trusting them. That's a different risk profile than gold in your own safe.

Gold-backed debit cards are best thought of as a convenience layer, not a liquidation strategy. For covering a dinner or a small purchase, they work. For converting a meaningful portion of your stack to cash? Probably not the move.

The Stuff Nobody Tells You

Bid-Ask Spreads Are the Real Cost of Selling

Here's a concept that trips up a lot of new stackers: the bid-ask spread.

When you buy gold, you pay the “ask” price — spot plus a premium. When you sell gold, you receive the “bid” price — spot minus a discount (or sometimes at spot, rarely above for standard bullion).

The difference between what you paid and what you can sell for is the spread. And it's the single most important number in determining whether your gold has actually made money.

Say you bought a 1 oz coin at $2,100 when spot was $2,000. You paid a $100 premium (5% over spot). Now spot is $2,100. You think you've broken even, right?

Not even close. If a dealer buys it back at 2% below spot, they're paying you $2,058. You paid $2,100. You're down $42 even though spot went up $100.

This is why cost basis tracking matters. Your real break-even isn't spot — it's spot plus the premium you paid, plus whatever the spread costs you on the way out.

Timing Matters, but Not the Way You Think

Everyone wants to sell at the top. Nobody does. That's just reality.

But timing does matter in a practical sense:

- Sell into demand, not into panic. When prices are rising steadily and physical demand is strong, dealer buyback prices tighten (better for you). When prices crash and everyone's selling, spreads blow out.

- Day of the week matters. Some dealers have better cash flow on certain days. Fridays are often slower.

- Time of day matters. Markets move during trading hours. Getting a quote at 10am Eastern on a Tuesday is very different from getting one at 4pm on a Friday when London's already closed.

- Don't sell on a day spot is dropping hard. Dealers widen their margins on volatile days to protect themselves. Wait for a calm day.

Know Your Tax Situation Before You Sell

In the US, physical gold is classified as a collectible. Long-term capital gains on collectibles are taxed at up to 28% — higher than the 15–20% rate on stocks and bonds. Short-term gains (held less than a year) are taxed as ordinary income.

I'm not a tax professional and this isn't tax advice. But I will say this: know your cost basis before you sell. Know what you paid, when you paid it, and what your holding period is. The difference between a 15% tax hit and a 37% tax hit can be thousands of dollars on a meaningful sale.

So What's the Actual Playbook?

If I had to boil it down:

- For small amounts or quick needs: Local dealer. Walk in, walk out, cash in hand. Accept that you'll give up 2–5% below spot on standard bullion.

- For larger amounts where you can wait: Get quotes from both local dealers and online buyback programs. Compare the net after shipping and fees. Go with whoever gives you more.

- For getting the best price and you're not in a hurry: Peer-to-peer. Build reputation over time so that when you need to sell, you already have it.

- For day-to-day spending from your stack: Gold-backed debit cards work, but mind the fees and track the tax events.

- For everything: Know your cost basis. Know what you paid, know what spot is, and know what the spread is going to cost you. Don't guess.

Buying gold is the easy part. Everyone loves buying. It's satisfying, it's tangible, you get to hold something real.

Selling is where the actual financial outcome gets determined. And most stackers don't think about selling until they have to — which is exactly when you make the worst decisions.

Think about your exit before you need one. Know who you'd sell to, how the process works, and what it'll cost. Your future self will thank you.

Want to understand why selling your gold too early might be the wrong move? Read: Stop Trying to Spend Your Gold — the philosophical case for holding.

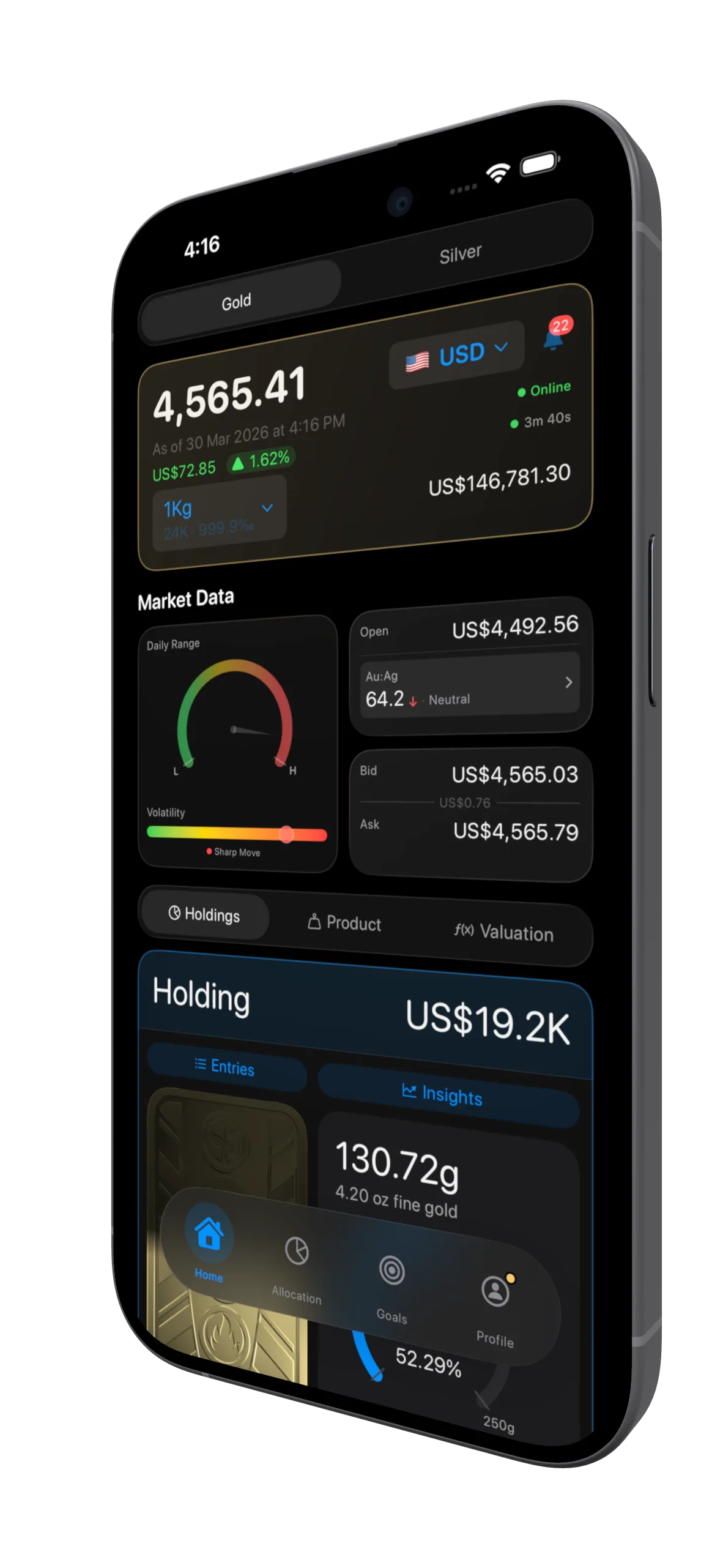

Know Your Cost Basis Before You Sell

BullionCoin Network calculates your real P&L across every purchase — premium paid, current spot, cost basis per gram — so when it's time to sell, you know exactly where you stand. No guessing, no spreadsheets.

Portfolio Overview

Portfolio Performance